Your gateway to organizational growth

Explore related insights or solutions.

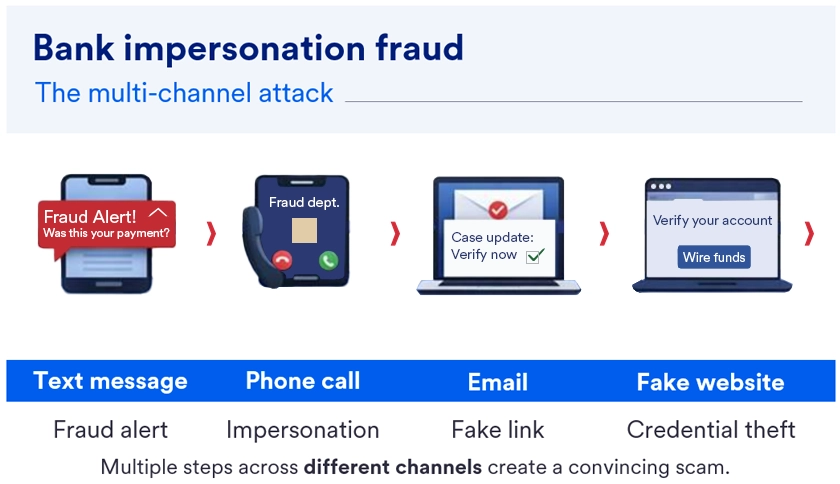

Bank impersonation scams are no longer single phishing attempts; they now operate as coordinated campaigns that use texts, phone calls, emails, and fraudulent websites to manipulate victim trust.

Attack sophistication is increasing, driven by generative AI, multichannel delivery and faster payment methods that are harder to reverse.

Corporate and commercial organizations are prime targets, particularly treasury, finance and payments teams with authority to move funds.

The strongest defense is layered: employee awareness, verified call‑back procedures, strong payment controls, and rapid response to unusual activity.

Social engineering fraud continues to be one of the fastest‑growing threats facing businesses. Rather than attacking systems directly, criminals exploit human behavior – urgency, authority and trust – to bypass technical controls.

Among social engineering fraud tactics, bank impersonation has surged because it leverages a powerful trust relationship: the one you have with your financial institution. Attackers increasingly mimic the language, branding and tone of legitimate bank fraud alerts to create interactions that feel routine, credible and urgent.

Recent reporting shows phishing and spoofing remain the most commonly reported cybercrime types, with overall fraud losses continuing to climb year over year. What has changed is how attacks are executed – they are now structured as end‑to‑end experiences rather than isolated messages.

"Cross-channel reinforcement is what makes modern fraud attacks so effective.”

Today’s bank impersonation scams are deliberately multistep and multichannel, designed to reinforce credibility at each stage. Here’s what a typical campaign flow looks like:

1. Initial contact (text or email). A message appears to come from the bank: “Unusual payment detected. Reply YES to confirm.”

2. Escalation (phone call/vishing). If the recipient responds or clicks, they receive a call from someone claiming to be a bank fraud specialist – often with spoofed caller ID.

3. Credibility building. The caller references partial real information (business name, address, recent transaction details) to build confidence.

4. Action request. The victim is instructed to:

5. Pressure and persistence. Follow‑up calls and messages keep urgency high and discourage independent verification.

This cross-channel reinforcement is what makes modern attacks so effective.

Several trends are increasing both the success rate and impact of bank impersonation fraud:

1. Generative artificial intelligence (AI) and synthetic media. Criminals are using AI tools to create more polished, convincing messages and scripts.

2. Interactive, guided scams. Rather than sending a single message, attackers now walk victims through a sequence of steps – mirroring legitimate fraud prevention workflows.

3. Faster, harder‑to‑reverse payments. Scammers increasingly push victims toward payment methods that settle quickly, reducing the opportunity to stop or recover funds once authorized.

Corporate and commercial organizations are especially attractive targets for these social engineering fraud attacks because:

Attackers study internal workflows and time their outreach to coincide with busy periods, leadership travel or end‑of‑day processing.

The most effective protection strategies align people, process and technology.

A treasury analyst receives a text claiming to be from the bank about a suspicious wire. After replying, the analyst receives a call from a “fraud investigator” who references real company details and urges immediate action to “secure funds.” Correct response:

Bank impersonation campaigns are successful because they move faster than normal business processes. The goal of your controls and training is to slow attackers down while speeding verification up.

By reinforcing consistent call‑back habits, strengthening payment controls and maintaining clear escalation paths, businesses can significantly reduce their exposure – without disrupting day‑to‑day operations.

For additional fraud prevention measures, read our comprehensive fraud prevention checklist.

Cyber threats aren’t going anywhere. At U.S. Bank, we offer in-depth knowledge and advanced solutions tailored to your needs. For specialized assistance and to learn more about protecting your organization, schedule a meeting with U.S. Bank experts.

Social engineering is a form of cybercrime where fraudsters manipulate people into revealing confidential information or performing actions that compromise security. Instead of hacking systems directly, these criminals use psychological tactics – posing as trusted partners, vendors or even bank employees – to trick you or your team.

1. Business email compromise (BEC)

A scammer hacks or spoofs a legitimate business email account (like a CEO, vendor or finance team member) and sends a convincing email to someone in the company – often someone in finance or HR – asking for a wire transfer, gift cards or sensitive data. The request often seems urgent and routine, so the victim doesn’t question it.

2. Vendor email compromise (VEC)

A scammer hacks into a vendor’s real email account or creates a lookalike (spoofed) email address. The scammer then sends a legitimate-looking invoice or payment request to a company that regularly does business with that vendor. The goal of the scam is to get the company to send money to a fraudulent bank account – often without realizing anything’s wrong until much later.

3. Phishing, vishing, smishing and quishing

4. Spoofed bank websites

Criminals create websites that closely mimic legitimate financial institutions, tricking users into entering login details or making payments. Always use saved, bookmarked site information to connect to your bank. .

Funds transfer fraud occurs when a fraudster initiates or alters a payment (e.g., wire, ACH, RTP) without the customer’s authorization by compromising systems, credentials, or payment instructions.

Key characteristics:

Social engineering fraud occurs when a fraudster manipulates or deceives a person into voluntarily authorizing a payment or disclosing sensitive information under false pretenses.

Key characteristics:

Explore proactive fraud prevention tools that banks have developed to help protect your organization from cyber threats.

Learn about fraud protection for payments processing your organization can implement to stay safe in the ever-evolving landscape of financial fraud.

Unlock timely, actionable strategies and perspectives from U.S. Bank experts — delivered straight to your inbox.