Article

How the U.S. healthcare system is shaping the economy

June 17, 2026

Key takeaways

Healthcare is taking on an increasingly important role in the broader U.S. economy.

A combination of an aging U.S. population and insufficient labor force growth is creating margin pressures for the industry.

Improving productivity – particularly through more effective technology use and labor efficiency – will be critical for maintaining profitability over the long term.

Healthcare is one of America's most prominent industries, yet it faces significant challenges due to unfavorable labor-force demographics and slower productivity gains. Healthcare touches nearly every corner of the U.S. economy, from household budgets to employer benefit costs to public spending. As its footprint grows, small shifts in costs, staffing and efficiency can ripple far beyond hospitals and clinics.

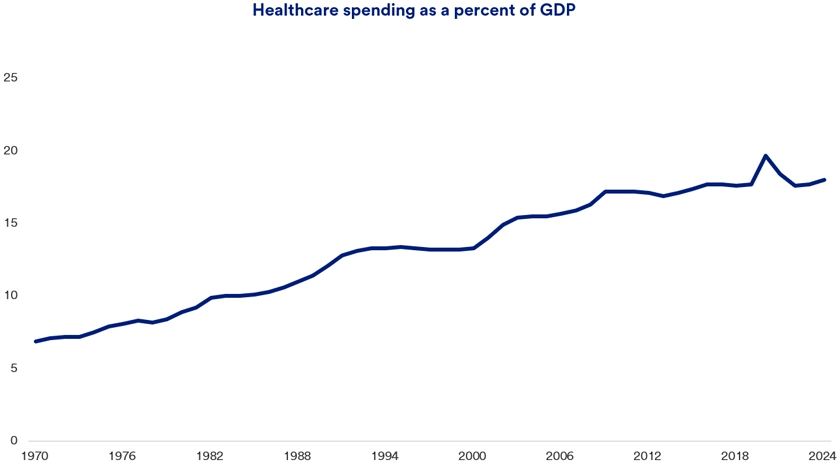

Healthcare spending accounted for 18% of the U.S. Gross Domestic Product in 2024, a figure expected to increase to 20% by 2033.1Spending grew by 7% annually in both 2023 and 2024. 1 Given the industry’s significant influence on the macroeconomic landscape, its challenges can have broader effects beyond the healthcare sector.

The U.S. healthcare system faces ongoing issues with affordability, structural labor shortages, and sluggish productivity growth compared to other economic sectors. These dynamics are contributing to margin pressures across hospitals, physician practices, and health insurers alike. Productivity growth is widely seen as essential for improving profit margins.

Although resolving cost and labor pressures may take time, there are reasons for cautious optimism. Policy tools, especially those involving insurance coverage, reimbursement structure, and workforce rules, have the potential to generate incremental improvements.

Perhaps even more important is effective technology implementation. Artificial intelligence (AI) and automation tools show early promise in reducing administrative burdens, improving staffing allocation, and supporting clinical decision-making. Continued investment in graduate medical education, if maintained, could also increase the supply of healthcare professionals. However, this factor has a longer development period, as the pipeline of medical graduates takes years to materialize.

“The reality of today’s aging U.S. demographics is that healthcare demand continues to grow,”

Beth Ann Bovino, chief economist, U.S. Bank

Healthcare’s role in U.S. labor market growth

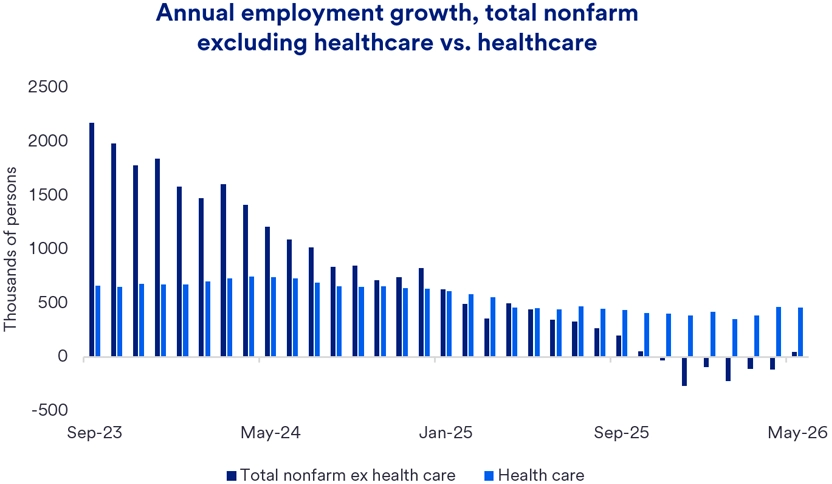

In recent years, the healthcare sector has emerged as the key driver of U.S. employment growth. In 2025, overall hiring remained relatively flat, but employment in healthcare increased by over 2%. There were 387,000 new healthcare jobs added in 2025, compared to a total growth of 116,000 jobs across the U.S. economy.2 Taken together, this implies that employment outside of healthcare experienced net declines in 2025.

“The reality of today’s aging U.S. demographics is that healthcare demand continues to grow,” says Beth Ann Bovino, chief economist at U.S. Bank. This shows that healthcare spending tends to rise as people get older. While making up only 30% of the U.S. population, Americans age 55+ accounted for 57% of total healthcare spending in 2023. 3

It's also notable that, in line with broader demographic trends of an aging population, that also means more doctors, nurses, and other healthcare professionals are aging out of the workforce, says Bovino. “That puts added pressure on the healthcare system.”

Read the full report

Healthcare and the U.S. economy: Structural pressures, labor constraints and the productivity imperative

Demographic headwinds facing the U.S. healthcare system

An aging population’s increasing demand for healthcare, along with the aging workforce in healthcare, creates a backdrop of specific supply-side constraints that have become more severe in recent years. “The healthcare sector has faced labor shortages for some time,” says Andrea Sorensen, vice president and economist at U.S. Bank. “An aging workforce and limited growth in the supply of healthcare workers are placing sustained pressure on the healthcare labor market.”

Historically, immigration played an important role in easing these pressures. Internationally trained physicians and nurses have helped expand the healthcare workforce, particularly in underserved and rural areas. However, that pipeline is now under threat. Between 2023 and 2025, new and continuing H-1B visas for health care and social assistance were up nearly 8% – from roughly 18,000 to over 19,000 – but a new $100,000 federal fee on H-1B petitions is expected to reverse that trend, hitting rural communities, low-income areas, and smaller employers hardest.4 “In the past, immigrants played a role in supplying doctors and nurses,” says Bovino, “That isn’t likely to be a big source for fill labor gaps in the coming years.”

The pipeline of healthcare professionals faces another obstacle as the number of residency positions has not kept up with population growth and the country’s aging trend. This restricts the potential number of new physicians. Nursing education faces similar challenges, including faculty shortages and limited clinical training capacity.

With a shortage of professionals, wage growth for physicians, nurses, support staff, and administrative workers currently exceeds broader wage increase averages. Because the healthcare sector is labor-intensive, these wage pressures often lead to higher prices, which further fuels already elevated healthcare inflation. 2

“Healthcare’s labor problem is not new,” says Sorensen. “Demographic trends have made this evident for some time. Given current conditions, labor shortages are likely to continue.”

Boosting productivity in the U.S. healthcare system

One way to address the impact of fewer available professionals is for healthcare providers, such as hospitals and physician practices, to implement productivity improvements. Although there are many challenges in measuring productivity for services in general and healthcare specifically, existing evidence shows that healthcare has experienced slower observable productivity growth compared to other service sectors. “Regulatory burdens often come into play in the healthcare sector,” says Sorensen. “There are opportunities where AI and other technological advances could boost productivity, once regulatory hurdles are overcome.”

Structural features help explain the sector’s productivity challenges. Existing payment systems usually reward volume rather than efficiency. Fragmented delivery systems often lead to duplicated tests and poor coordination among providers. Information systems are often isolated, which reduces communication between providers. Additionally, providers spend significant time fulfilling regulatory and administrative requirements. In many markets, limited competition decreases the pressure to improve efficiency.

Technology advancements, many of which are AI-related, hold the greatest productivity enhancement potential. The most immediate productivity gain opportunities include reducing administrative burdens, enhancing scheduling and capacity management, and supporting clinical decision-making. Larger providers may have an advantage in adopting new technologies, which could further widen existing gaps with smaller providers. “Adding more technology training to the list of skills that associates must learn is another major hurdle to achieving productivity improvements,” says Matt Schoeppner, senior economist at U.S. Bank. “The challenge isn’t limited to the healthcare sector, but it tends to be more evident there.”

Overcoming margin pressures in the healthcare system

Margin pressures exist throughout the healthcare system. However, they tend to affect different industry participants in different ways.

Hospitals

Hospitals face significant margin pressures. Labor costs are the largest expense and the most persistent challenge. Due to the labor-intensive nature of hospital operations, productivity growth has been limited. Ongoing workforce shortages push wages higher. A major challenge hospitals encounter is the ability to pass on rising costs to payers. This is especially true in markets with a high share of public payers, where reimbursement rates are set and tend to lag behind input inflation.

While productivity improvements can boost profitability, quick implementation is challenging in a hospital setting. Despite substantial technology investments, many hospitals have mainly achieved administrative efficiencies rather than measurable clinical outcome improvements. In the short term, productivity efforts are more likely to help stabilize margins rather than significantly grow them.

Hospitals also face risks due to recent cutbacks in Affordable Care Act (ACA) subsidies and reduced Medicaid enrollment. “Hospitals are federally required to provide emergency care, regardless of the patient’s ability to pay,” notes Sorensen. “This can result in increased unreimbursed care. Most at risk are hospitals serving lower-income populations where insurance coverage is spottier.” Sorensen says hospital systems concentrated in higher-income, commercially-insured markets are more insulated from these cost pressures.

Physician practices

Physician practices face labor pressures similar to those of hospitals, but their margin dynamics differ. Smaller practices lacking scale experience significant cost pressures due to rising labor expenses. The same applies to independent practices with limited ability to negotiate with insurers and fewer resources to absorb cost shocks. These cost pressures often lead to the consolidation of independent practices with larger groups or hospital-owned practices.

A benefit for physician practices is reduced exposure to unpaid care compared to the pressures hospitals face. Practices usually require patients to show they have insurance coverage or can prepay for services. Cuts to ACA subsidies may affect patient volume but are unlikely to impact profit margins.

A benefit for physician practices is reduced exposure to unpaid care compared to the pressures hospitals face. Practices usually require patients to show they have insurance coverage or can prepay for services. Cuts to ACA subsidies may affect patient volume but are unlikely to impact profit margins.

Physician practices may be more conducive to productivity improvements. Automating tasks like scheduling, coding, documentation, and prior authorization can reduce overhead costs. AI-powered tools that ease administrative tasks can boost effective per-physician output. Even if reimbursement rates remain steady, increased productivity can help preserve profit margins.

Insurers

Insurers face a different set of concerns compared to providers. If hospitals and physician practices raise their fees to cover rising costs, insurers might respond by increasing coverage premiums. However, their ability to do so could be limited, especially in regulated markets like ACA exchanges.

ACA subsidy reductions significantly affect insurers in the individual market. The removal of enhanced subsidies may lead healthier enrollees to drop their coverage. This results in a smaller overall membership and a less healthy risk pool under ACA coverage. The overall effect could be higher premiums for ACA participants or narrower profit margins for insurers, or both. Margins in this segment of the insurance market were already thin, so even moderate shifts in enrollment or risk mix could disproportionately affect earnings.

Insurers face less risk from uncompensated care than providers, with margin concerns mainly influenced by enrollment mix, utilization patterns, and pricing discipline.

Insurers have also made significant progress in using data analytics to increase productivity. Technological advancements, including AI-driven risk assessment, can help reduce administrative costs and improve profit margins. However, these tools work within regulatory and reputational constraints. Over time, insurers may be well-positioned to effectively adopt these technologies to address cost pressures.

Challenges and opportunities for U.S. healthcare system

A combination of challenging demographic trends and slow technology adoption as a way to boost productivity create margin pressures within the healthcare sector. Labor pressures stemming from growing demand and an aging workforce are most evident among hospitals and physician practices. “Despite the challenges, this sector remains a major component of the U.S. economy,” says Sorensen. “This is driven in large part by increasing demand for health care services.”

Physicians might be better positioned than hospitals to implement productivity improvements that offset adverse demographic trends. Insurers face increasing medical costs and enrollment risks, especially in individual markets. They have greater flexibility to adjust prices, manage utilization, and diversify risk.

A reality for the industry is that labor costs remain elevated and reimbursement growth is constrained. It’s crucial for healthcare firms to use technology to cut administrative barriers, deploy staff more effectively, and increase productive output.

The primary focus for most healthcare entities is less about expanding margins than taking steps to maintain current profit levels. Uncovering productivity enhancements is critical in preventing margin erosion.

The U.S. healthcare system and the economy

Healthcare spending in the U.S. accounted for 18% of U.S. Gross Domestic Product (GDP) in 2024, the most recent year for which data is available. It is projected that healthcare spending will increase to 20% of U.S. GDP by 2033.1 Given that prominent role, healthcare-related jobs are also on the rise. In 2025, while overall hiring remained relatively flat, healthcare employment increased by more than 2%, with nearly 400,000 new healthcare jobs added in that year.2

The U.S. healthcare system’s expanding role in the economy

As recently as the early 1980s, healthcare accounted for less than 10% of the economy based on GDP. It has steadily increased since then, briefly reaching just under 20% of GDP in 2020, the year the COVID-19 pandemic began.1 According to the Center for Medicare & Medicaid Services, total healthcare spending was $322 billion in 1982, or $1,365 per person, and it now totals $5.3 trillion, or $15,474 per person.

Factors shaping healthcare costs and spending

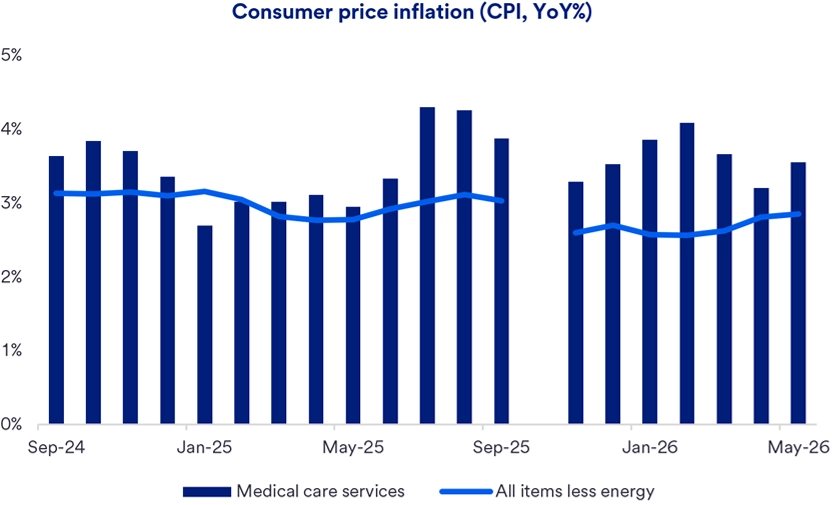

According to the U.S. Bureau of Labor Statistics, healthcare costs in 2025 and 2026 increased more quickly than overall consumer price inflation. As of May 2026, the Consumer Price Index excluding energy for the past 12 months rose by 2.86%, compared to 3.56% for healthcare inflation. Several factors contribute to healthcare costs growing faster than overall inflation. These include increasing demand for services, largely due to aging demographics. Although Americans age 55+ make up only 30% of the U.S. population, they accounted for 57% of total healthcare spending in 2023.3 The need for more healthcare workers to meet this rising demand also adds to price pressures.

Labor and productivity as constraints on healthcare system

As America’s population ages, many healthcare professionals are approaching retirement age, creating pressure to find enough workers to replace them. Increasing U.S. government immigration restrictions might limit one potential source of new healthcare workers—internationally trained physicians and nurses. Another challenge for the industry is that it tends to lag behind the overall economy in productivity improvements. While artificial intelligence and other technological advances could help boost productivity, the healthcare industry might face more regulatory hurdles than other sectors before those tools can be implemented.

Tags:

U.S. Bank Economics Research Group

Beth Ann Bovino

Chief Economist

Ana Luisa Araujo

Senior Economist

Matt Schoeppner

Senior Economist

Adam Check

Economist

Andrea Sorensen

Economist

Subscribe to our economic insights newsletter

Not currently a subscriber? Sign up to get our economic insights delivered to your inbox weekly.

Learn more

If you have any questions about any of these topics or want to learn more, please contact us to connect with a U.S. Bank Corporate and Commercial banking expert.