Capitalize on today’s evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

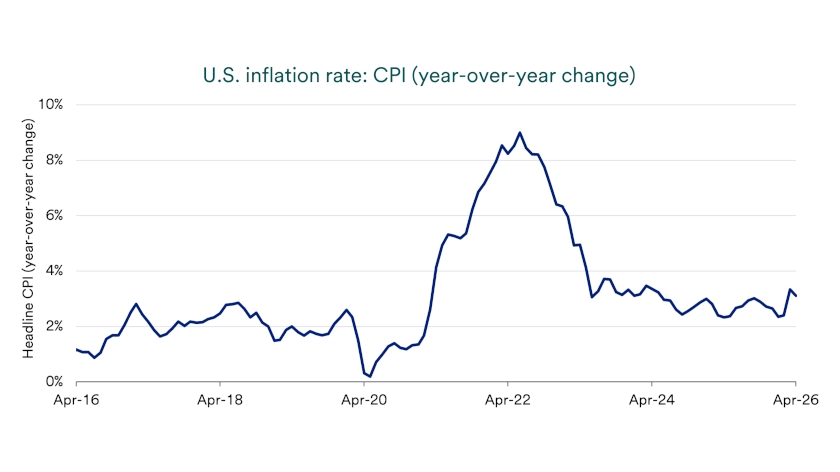

April year-over-year inflation rose to 3.8% as higher energy prices pushed headline numbers higher.

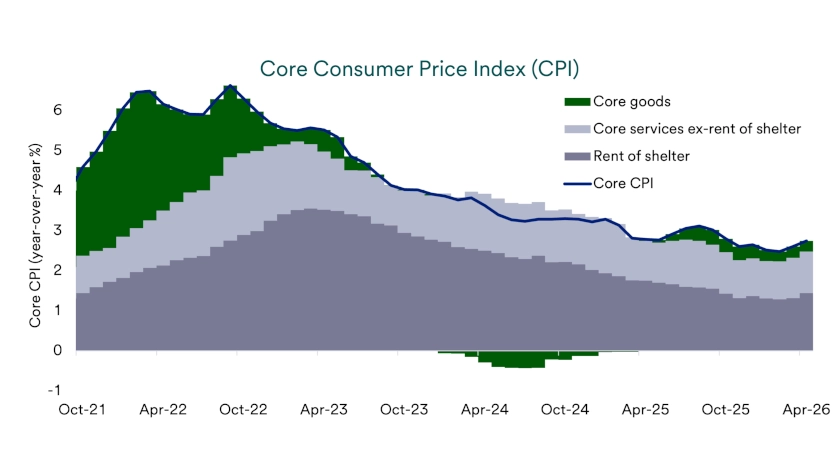

Core inflation stayed lower at 2.8%, and slower shelter cost increases may still help ease price pressure over time.

The Federal Reserve and investors will watch energy, tariffs, and future inflation reports to gauge when interest rates may fall.

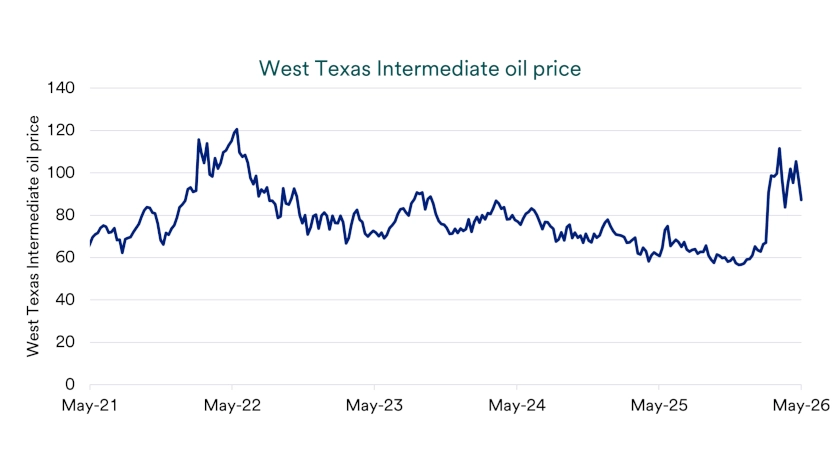

Current inflation affects the economy by raising the cost of living, influencing interest rates, and shaping investment decisions. The March 2026 Consumer Price Index (CPI) rose 3.8% over the past year as energy costs jumped in April. Household budgets also face pressure from service costs, which kept core CPI, excluding food and energy, elevated at 2.8% year over year. 1 Investors also watch the Bureau of Economic Analysis’ Personal Consumption Expenditures (PCE) price index because the Federal Reserve uses it in defining its inflation target, and April’s Core PCE price index rose 3.3% versus the prior month’s 3.2% increase. 2 More recently, investors have focused on what comes next as oil transportation constraints in the Middle East push energy prices higher and raise concern about future inflation.

Headline CPI increased 3.8% over the past 12 months in April compared to 3.3% in March. Core CPI, which removes food and energy to show the underlying trend, rose 2.8% from a year earlier, above the 2.6% reading in March. 1 In plain terms, the energy price spike tied to the Iran conflict is lifting headline inflation, while core prices show modest increases so far. Even so, inflation remains high enough that interest rate expectations can change quickly as new data arrives.

Energy drove most of March’s jump in prices, but other factors related to services placed upward pressure on inflation as well. The shelter index rose 3.3% over the past year, while utility costs and transportation each rose over 4.0% year-over-year. 1 Even with mortgage rates still elevated, housing-related inflation usually takes time to cool. Over time, stable to lower home prices, mortgage rates, and rents should help ease shelter inflation and offset some pressure from higher goods prices.

Shelter inflation changes often update slowly in the official data because leases reset gradually rather than all at once. In a December 15, 2025 speech, Fed Governor Stephen Miran explained that the Fed’s preferred PCE shelter index lags market rents because rents usually reset when people move or renew leases. He said the earlier “catch‑up” in measured shelter inflation is largely complete and described current elevated readings as an after‑echo of past imbalances. That view supports the case that shelter inflation could fall faster as the data catch up to today’s slower rent growth. 3

Geopolitical conflict can push inflation higher when it disrupts energy supply or raises shipping and insurance costs. Higher oil and gasoline prices can lift headline inflation quickly, and they can also raise costs across transportation and supply chains before those increases reach consumers. If energy costs stay high, they can weigh on consumers and businesses at the same time as each must adjust to higher costs without extra income. That mix makes the outlook more difficult for markets and policymakers.

“Markets are sensitive to sustained, accelerating inflation, but underlying inflation ex-energy has been modest in recent months,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. However, Haworth warns that inflation is not the only trigger for market volatility, adding, “Labor market weakness could suggest higher economic slowdown odds, which would represent a material market development, although recent labor market data has been encouraging.”

“Markets are sensitive to sustained, accelerating inflation, but underlying inflation ex-energy has been stable to lower in recent months. Further labor market weakness may suggest higher economic slowdown odds, which would represent a material market development, although recent labor market data has been encouraging."

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

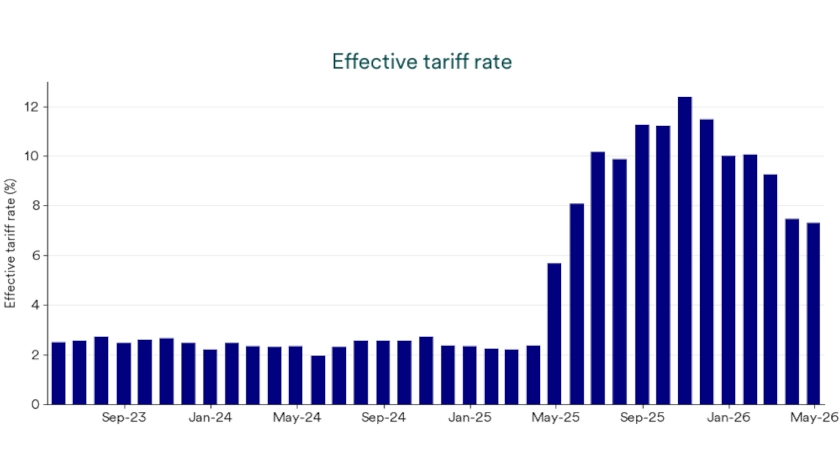

Tariffs remain an important wild card for inflation because they can raise the cost of imported goods and the materials used to make them. Recent legal and policy developments have added more uncertainty. The Supreme Court ruled that President Trump cannot impose tariffs under the International Economic Emergency Powers Act (IEEPA), which canceled most of the 2025 tariffs tied to that authority. After that ruling, the administration announced a temporary 15% global tariff under Section 122 of the Trade Act of 1974 while it considers other options.

Even if headline tariff rates change, the overall tariff burden could remain meaningfully higher than it was in 2024. One way to track that burden is the “effective tariff rate,” which estimates the average tariff cost by comparing customs revenue to the total value of goods imports. Businesses can absorb part of that cost, pass part of it to consumers, or shift supply chains, so tariffs can affect inflation unevenly and with a delay. “Investors watch inflation closely because of the impact on personal budgets, although the effective tariff rate fell considerably after the Supreme Court struck down certain tariffs earlier this year,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group.

The Personal Consumption Expenditures price index matters because the Federal Reserve uses it as the benchmark for its 2% inflation goal. In April, the PCE price index rose 3.8% from a year earlier. Excluding food and energy, PCE prices rose 3.3% over the past year. 2 Those readings help explain why some members of the Fed have been increasingly cautious when speaking about interest rate policy until they see stronger evidence that inflation is moving lower. 3

Other economic data highlight why inflation can trend higher at the same time as consumer demand. Consumer spending metrics indicate strength, with retail sales near 5% growth and certain alternative measures capturing data through May suggesting even higher increases in spending. 4 When households keep spending, especially on services, prices can remain firmer in the parts of the economy that usually cool last. That dynamic can keep inflation from returning to target as quickly as investors might hope.

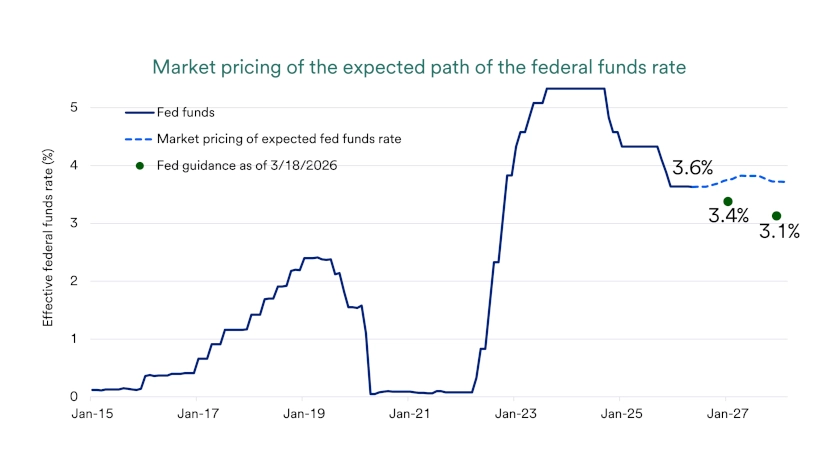

Higher energy costs and inflation metrics have prompted some members of the Federal Reserve to highlight two-sided risks to policy rates, implying they may prefer to increase rates if inflation remains problematic. Interest rates price in over 50% odds of a 0.25% policy rate increase by the end of 2026 versus the current range of 3.50% to 3.75%. That marks a notable shift compared to earlier in the year before the conflict in Iran when interest rate markets priced in as many as two rate cuts in 2026. 5

Shifting expectations around Fed policy highlights the important relationship between inflation and monetary policy, with geopolitical factors including energy supply heavily influencing the path of interest rates in 2026. The pace of inflation improvement, along with the growth backdrop, will likely determine whether rate cuts resume or remain limited. Investors should expect this outlook to keep changing as new reports are released.

Inflation matters to investors because it can reduce the real value of portfolio growth over time. Even when an account balance rises, those gains may buy less if the cost of goods and services continues to increase. For long-term investors, the goal is not only to grow assets, but also to preserve purchasing power.

Inflation can also influence interest rates, which can affect both bonds and stocks. When rates move higher, older bonds with lower yields often lose value in the market. Higher rates can also weigh on stock prices by reducing the present value of future earnings. A diversified investment strategy can help investors manage these risks while staying focused on long-term growth.

Inflation reduces purchasing power by making everyday goods and services more expensive over time. As prices rise, each dollar buys less than it did before. This gradual change can affect household budgets, retirement planning, and long-term savings goals.

The long-term impact can be significant. Based on the Consumer Price Index from the U.S. Bureau of Labor Statistics, something that cost $1 at the start of 2000 cost about $1.93 by the start of 2026. That means prices nearly doubled over that period, showing why inflation remains an important part of financial planning and investment strategy.

Inflation explains the difference between nominal returns and real returns. A nominal return is the number shown on an investment statement, paycheck, or savings account. A real return adjusts for inflation and shows how much buying power actually increased after rising prices are taken into account.

For example, a bond may pay a 5% nominal yield over a year. If inflation averages 2% during that same period, the real return is closer to 3%. Investors track this difference because strong long-term results depend on growing wealth faster than the cost of living.

Many people notice inflation when prices jump in a given month or year. Investors usually focus on inflation as a long-term risk because prices tend to rise over time, even when inflation slows for a period. That steady increase can gradually reduce the future value of savings and investment gains.

For long-term investors, inflation is not just a short-term headline. It is an ongoing part of portfolio planning, retirement income planning, and wealth preservation. A sound investment approach aims to outpace inflation over time so investors can maintain spending power and stay on track toward long-term financial goals.

The best response to an uncertain inflation path is to stay focused on what you can control. Inflation remains a key driver of interest rates and market volatility, and tariffs and energy shocks can create short-term setbacks even when the longer-term trend is improving. A disciplined plan and a broadly diversified portfolio can help investors avoid making lasting decisions based on a single report or a short burst of volatility. That approach can keep long-term goals at the center of the plan.

If inflation continues to cool, especially if shelter inflation keeps easing with a lag, the case for lower rates can strengthen. If energy prices rise sharply or tariffs become more inflationary than expected, that timeline can shift. Talk with your financial professional about how your portfolio aligns with your goals, time horizon, and comfort with short-term swings, and discuss whether any adjustments make sense for your situation.

In April 2026, CPI increased 3.8% over the prior 12 months and rose 0.6% for the month. 1 Those figures reflect the average change in prices across a broad basket of goods and services. Inflation can still feel uneven because housing, food, and energy prices do not always move in the same direction as the overall average.

Core inflation removes food and energy because those prices can move sharply from month to month. In April, core CPI rose 0.4% for the month and 2.8% from a year earlier, which showed that underlying inflation pressure was still present. 1 Core measures can help investors see whether inflation is easing in the parts of the economy that tend to move more slowly.

The Federal Reserve has said it targets 2% inflation over time as measured by the Personal Consumption Expenditures price index. PCE can better reflect how consumers change what they buy when prices move, and it covers a broader set of spending categories. That is why PCE often carries more weight when investors think about the path of interest rates.

Federal Reserve calibrates monetary policy to help lower inflation.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.