Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Consumer spending continues to support U.S. economic growth, driven by steady wages, low layoffs and resilient household finances.

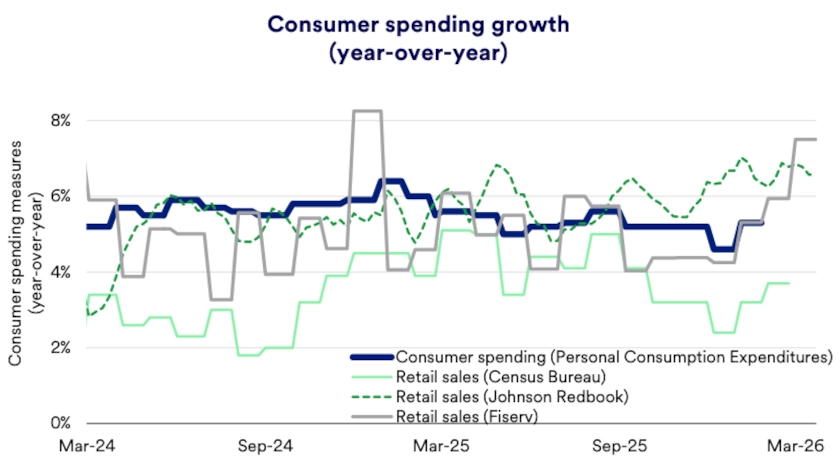

Retail sales show steady demand, with year‑over‑year growth led by services and online spending, even as monthly gains moderate.

Household debt remains manageable overall, as income growth and relatively low debt‑payment burdens help offset higher borrowing costs.

Consumer spending remains the backbone of the U.S. economy, accounting for approximately two‑thirds of total economic activity. 1 That scale gives household behavior an outsized influence in shaping U.S. economic growth, corporate earnings and investor confidence. As long as consumers continue to engage in the economy, expansion tends to persist, even when other parts of the economic cycle cool.

Recent data continue to show that consumers are participating in the economy even as the pace of growth becomes more measured. Households appear more selective about where dollars flow, yet aggregate demand continues to expand. This resilience helps explain why economic growth has remained intact despite softer confidence readings and tighter financial conditions.

“Consumer spending continues to benefit from steady income growth and a labor market that remains supportive.”

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

“Consumer spending continues to benefit from steady income growth and a labor market that remains supportive,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group.

The latest retail sales data reinforce the picture of a consumer that remains engaged. The U.S. Census Bureau reported that retail and food services sales rose 0.6% in February 2026 and increased 3.7% from a year earlier, signaling ongoing expansion in household demand. 2 Gains were broad enough to offset softness seen earlier in the winter, suggesting consumers continue to spend even as conditions evolve.

Several categories continue to lead year‑over‑year growth. Non-store retailers posted a 7.5% increase from February 2025, while food services and drinking places rose 5.2% over the same period. 2 These trends point to sustained demand for convenience, services, and experiences, even as higher prices encourage more deliberate purchasing behavior.

High‑frequency indicators tell a similar story. “Consumer spending proxies such as retail sales, credit and debit card swipes, restaurant bookings, and daily tax withholding statistics suggest aggregate consumer behavior remains solid,” according to Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. Fiserv’s point-of-sale data available through late March indicates year-over-year spending growth above 7%, while Johnson Redbook’s weekly retail sales data available through the third week of March indicates 6% year-over-year growth.

The conflict in Iran sent gas prices up over $1 per gallon in March. 3 If sustained, higher energy prices can crowd out spending on other goods and services, while contributing to broader inflation pressure. Tax cut legislation, passed last year, is projected to translate to an extra $50 billion in individual tax refunds on 2025 tax returns. 4 Cumulative incremental tax cuts should exceed extra spending on gasoline at current prices until mid-June, buying time for Middle East tensions to de-escalate. An extended closure of the Strait of Hormuz, however, would eventually strain households after tax stimulus offsets subside.

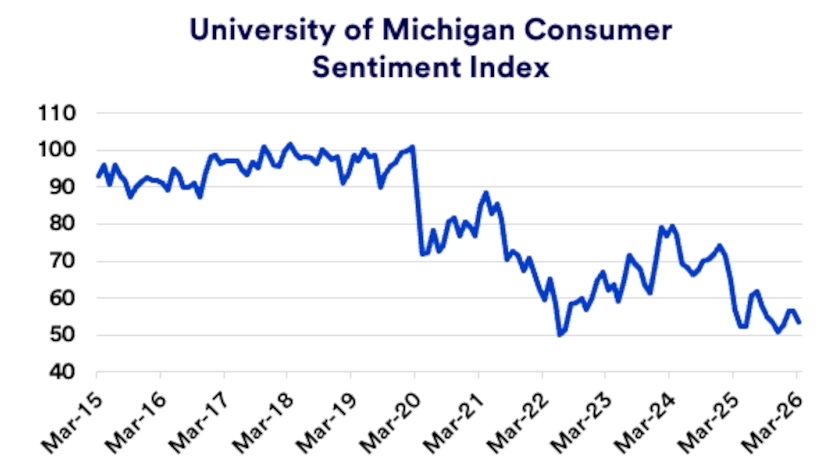

Measures of consumer sentiment continue to lag actual spending behavior. The University of Michigan’s March 2026 survey showed sentiment slipped from the prior month and year‑ago levels, reflecting persistent concerns around high prices and economic uncertainty. 5 Respondents generally cited elevated prices as a pressure on personal finances.

Confidence trends slipped across a wide variety of households. Higher‑income and asset‑owning consumers reported worse sentiment in the wake of the Iran conflict and higher gas prices. Lower‑income and non‑investing households remained cautious. The data pattern suggests consumers may not expect these challenges to persist far into the future.

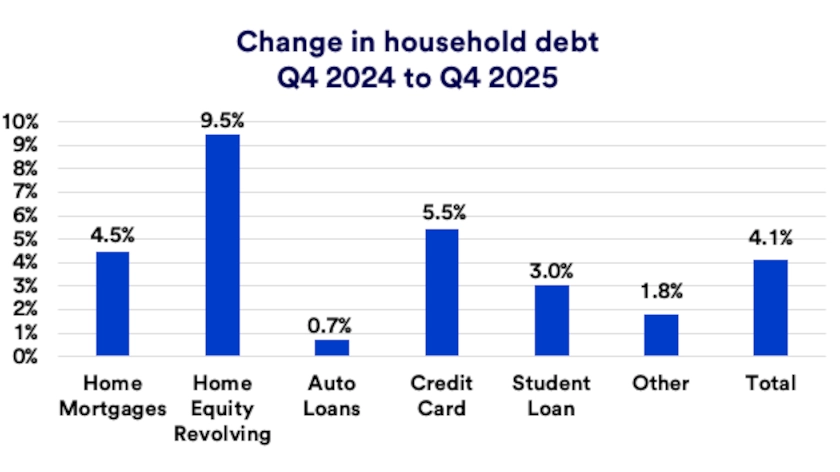

Household debt continues to rise, though the pace remains measured. The New York Federal Reserve reports that total household debt increased 4.1% in the fourth quarter of 2025, bringing outstanding balances to $18.8 trillion. 6 What matters most for consumer spending is not the total level of debt, but whether debt meaningfully changes household cash flow.

Credit card balances have increased more noticeably, rising in the fourth quarter to stand 5.5% higher than a year earlier. That trend can signal pressure for some households, especially as higher interest rates raise borrowing costs. Still, income growth remains an important offset. “A key to consumers maintaining healthy balance sheets is that income growth outpaces inflation,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. Nominal wages continue to exceed the cost of living, even as gains slow for lower‑income households.

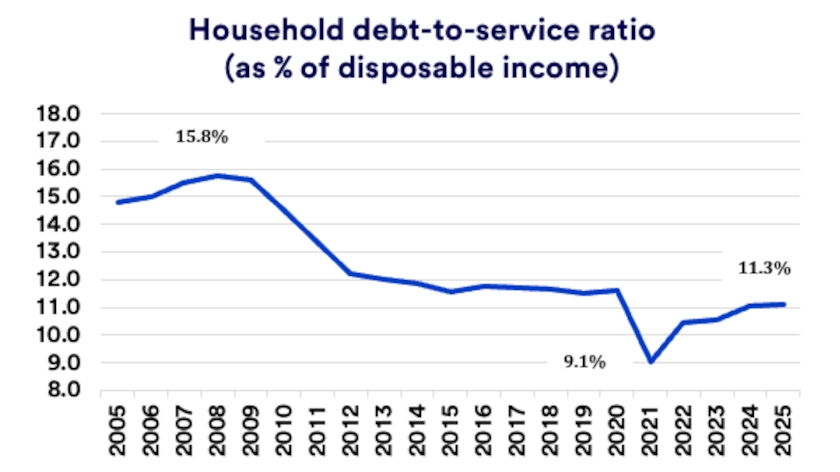

Debt affordability offers additional context. Household debt payments equal roughly 11.3% of disposable income, well below the 2007 peak of 15.8%. 7 That cushion suggests many households still maintain financial flexibility, even as higher‑rate borrowing creates pressure at the margins.

Labor market conditions remain an important pillar for consumer spending. Nonfarm payrolls increased by 178,000 in March 2026, while the unemployment rate fell to 4.3%, reflecting continued job creation even as hiring cools from earlier peaks. Job gains in healthcare, construction, and transportation continue to offset declines in federal government employment. 8

Weekly unemployment insurance data reinforce this picture of stability. Initial claims declined to 202,000 in the week ending March 28, and the four‑week moving average fell to its lowest level since late 2024, signaling limited layoff activity. 9 Low claims levels help preserve income continuity for households.

Wage growth also remains supportive. Average hourly earnings rose 3.5% over the past year, allowing incomes to keep pace with inflation and sustain purchasing power for many households. 8 “Income growth remains a key stabilizer for consumers as the labor market moves toward better balance,” says Hainlin.

Market performance has started to reflect these cross‑currents. Equity markets entered 2026 on firmer footing even as consumer‑oriented stocks lagged broader gains, reflecting expectations for slower but ongoing growth. Stable consumer spending continues to support corporate revenues despite tighter financial conditions.

Looking ahead, consumer behavior remains a central variable for investors. Steady spending, low layoffs, and ongoing income growth suggest households can continue to support economic expansion, even as growth normalizes. As Terry Sandven, chief equity strategist for U.S. Bank Asset Management Group, observes, “The durability of the consumer remains a key reason the broader economic outlook stays constructive.”

As always, investors should work with their wealth planning professional to ensure portfolios align with both current economic conditions and long‑term financial goals.

Consumer spending matters because it makes up approximately two‑thirds of U.S. economic activity and often drives short‑term economic growth. 1 It includes everyday purchases of goods and services, and government agencies track it closely as a key part of gross domestic product and as an early gauge of economic strength. When consumer spending holds up, it supports business revenue and hiring, which can help the economy keep expanding.

Retail sales trends suggest consumer demand remains steady overall. The Census Bureau’s retail and food services sales data rose 0.6% month‑to‑month in February while still running higher than a year earlier, which points to continued spending even as momentum cools. 2 Taken together, the data suggests households are shifting where they spend rather than stepping away from spending altogether.

Rising household debt can be a risk to consumer spending, but the impact depends on whether payments strain monthly budgets. Recent Federal Reserve Bank of New York data shows household debt rose modestly in late 2025, with credit card balances increasing alongside other categories. 6 Even so, broader measures that compare debt with income have remained relatively low by historical standards, which suggests many households still have capacity before debt becomes a widespread spending constraint.

Growth slowed late last year as the government shutdown weighed on activity, while consumer spending, hiring and income trends remained broadly supportive.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.