Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

Private credit can add income for investors, but access to cash depends on each fund’s redemption rules and timing.

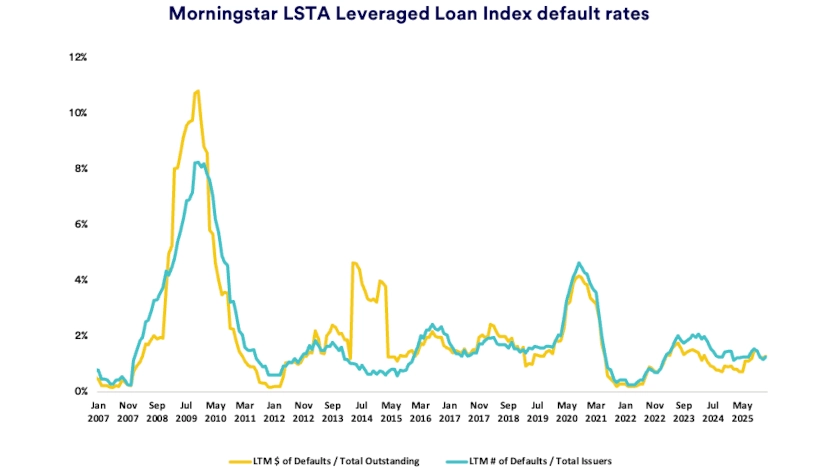

Defaults in widely held corporate loans remain relatively low, which suggests broader spillover may stay limited even as liquidity tightens.

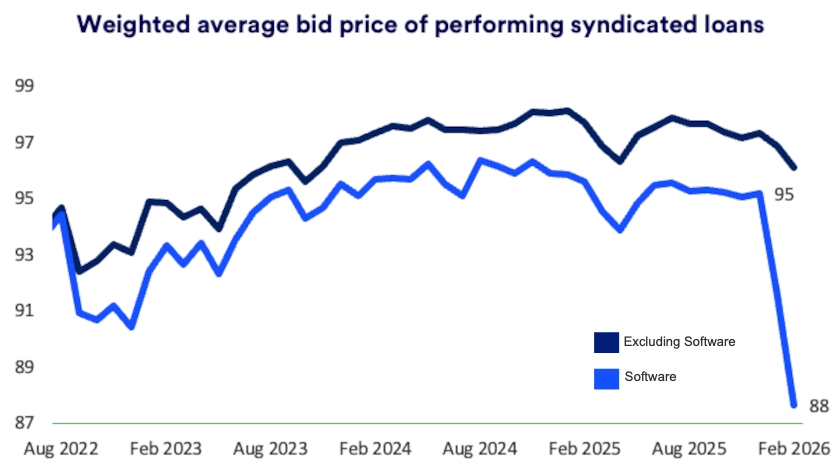

Stress looks most visible in software loans, where some debt trades below 80 cents, suggesting active credit management, diversification and senior, collateral-backed loans can help investors stay disciplined.

Private credit opportunities have expanded beyond institutions and into more investor portfolios, often through fund structures designed for individuals. That growth also exposed a basic constraint: many private loans trade infrequently, so selling them quickly can be difficult when markets turn volatile. Recent headlines have amplified these differences, making it important to separate questions about fund structure from borrower fundamentals.

Blue Owl, a business development company (BDC) that makes loans, generated headlines by limiting investor withdrawals in a non-traded private credit fund aimed at individuals 1. Reports described a shift to occasional payouts funded by repayments and asset sales, instead of limited quarterly redemption offerings. As a result, some investors may not be able to exit when they anticipated or prefer.

“The primary issue is a mismatch in terms between the underlying loans and the redemption features of many of these funds. If there is an event that leads to many investors requesting redemptions, these structures have difficulty fulfilling these requests from their natural sources of liquidity.”

Kaush Amin, head of private market investments for U.S. Bank Asset Management Group

“The primary issue is a mismatch in terms between the underlying loans and the redemption features of many of these funds,” said Kaush Amin, Head of Private Market Investments for U.S. Bank Asset Management Group. “If there is an event that leads to many investors requesting redemptions, these structures have difficulty fulfilling these requests from their natural sources of liquidity.” Loan terms are most often three to seven years, while investors can often seek redemptions quarterly. That timing gap becomes more visible when many investors request cash at the same time.

Public loan markets started 2026 under pressure, and that tone has influenced how investors view private credit risk. A passive fund tracking the Morningstar LSTA U.S. Leveraged Loan Index fell over 2% in February 2, and has 26% of capital invested in software loans, according to Bloomberg. This stood in stark contrast to the near-zero total return in February from below investment grade corporate bonds, which have a 3% weight to software. Debt from highly leveraged or smaller software companies came under pressure despite busy new loan activity as companies refinanced existing debt and financed mergers. This mix—softer secondary prices alongside heavy refinancing—signals that investors are becoming more selective rather than uniformly willing to take risk. 2 The divergence in performance also highlights the importance of diversification and active management when investing in credit-intensive assets.

At the same time, retail-oriented private credit vehicles are facing a more demanding liquidity environment. Fitch reported that redemptions for non-traded, perpetual BDCs that it tracks rose to an average of 4.5% of net asset value in 4Q25, up from 1.6% in 3Q25, alongside slower fundraising amongst funds. 3 However, in 1Q26, redemption requests for non-traded BDCs averaged 9% – 10% of net asset value, far exceeding the 5% redemption limits set by many of these vehicles. Net asset value is the fund’s estimated value per share, and higher redemption demand can limit cash exits in such semi-liquid vehicles holding illiquid loans.

The recent collapse of Market Financial Solutions Ltd. in the U.K. has added to the market’s focus on collateral quality and lending standards. The company sought administration, a formal insolvency process in the United Kingdom, after an unexpected banking-related issue temporarily restricted access to everyday banking facilities, even as it described its business as asset-backed. 4 Reuters reported that court documents raised concerns that the same assets served as collateral on multiple loans, referred to as “double pledging,” and warned of a possible collateral shortfall. 5 The situation echoes last year’s collapses of First Brands Group and Tricolor Holdings that also raised questions about collateral monitoring. 5

A practical way to gauge broader stress is to watch default rates in large, widely held corporate loans. As of January 31, 2026, the trailing 12-month default rate for below investment grade loans was 5.5% according to Moody’s, compared to a 3.4% default rate in high yield corporate bonds. 6 Loan defaults are somewhat above long-term averages, but still within normal ranges. High yield bond defaults are slightly below average, supporting a measured interpretation of today’s concerns.

Even when default rates remain contained, liquidity can tighten quickly in vehicles that offer periodic withdrawal windows. If redemption requests surge, a fund may need to sell less-liquid assets, and that selling pressure can create more headlines and more anxiety. This feedback loop can make stress feel contagious even when many borrowers continue making timely payments.

It also helps to keep the market’s scale in context. Public reporting has described private credit as having grown dramatically since the global financial crisis and reaching roughly the $1.8 trillion range globally. 7 A market of that size can draw intense attention when headlines question valuation practices or liquidity terms, even if loan performance varies widely from borrower to borrower. However, the size of the private credit market remains small relative to the traditional bond market in the U.S., which includes over $30 trillion of U.S. Treasuries, $11 trillion in corporate bonds, and $10 trillion of mortgage bonds according to SIFMA.

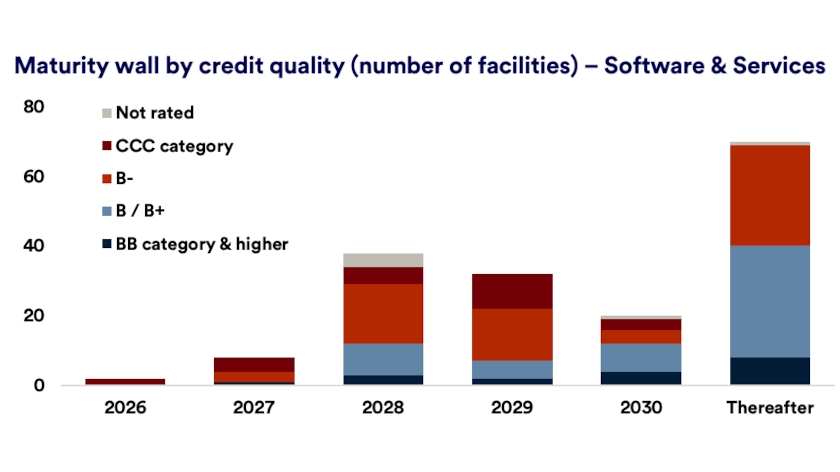

Current concerns cluster most visibly around software and services loans, where investors debate how artificial intelligence could reshape business models. 8 In the Morningstar LSTA US Leveraged Loan Index, Software & Services represented about 16% of outstanding debt as of early February, and more than half of the sector sat in the “highly speculative” part of the credit-quality scale (a Fitch rating of B-minus or below). 9 Those weaker ratings matter because refinancing can become harder if sentiment turns and lenders demand tougher terms.

Market pricing reflects that caution. The same analysis noted that about 21% of Software & Services loans traded below 80 percent of par value (less than $0.80 for each $1 of face value), and that a meaningful share of maturities fall in 2028 and 2029. 8 A price below 80 does not guarantee default, but it often signals investors are demanding a steep discount for refinancing uncertainty and reduced liquidity.

Another PitchBook analysis noted a record $25 billion of speculative-rated software loans trading below 80 cents as of January 31. 10 “Speculative-rated” generally means below investment grade, which can make borrowers more sensitive to tighter financing conditions. These pockets of stress can coexist with steadier conditions elsewhere, so diversification and security selection remain important.

Private credit can remain a constructive long-term portfolio allocation for qualified investors, especially when the strategy emphasizes downside protection and careful underwriting. The most important decision is often not whether to own private credit, but whether the manager, portfolio construction and liquidity design match an investor’s risk tolerance and time horizon. When loan maturity and investor liquidity expectations line up, investors can reduce the chance that a fund must sell assets at unfavorable prices.

Two definitions help keep risk discussions grounded. “Maturity” describes how long a loan lasts before the borrower must repay it, while “liquidity” describes how quickly an investor can convert an investment to cash without taking a large discount. Problems tend to arise when a fund offers frequent withdrawals but holds loans the fund cannot easily sell on demand, particularly during volatile markets.

Investors can also manage risk by favoring loans that sit closer to the front of the repayment line. “First lien” means the lender is first in line on pledged collateral if a borrower runs into trouble, while “senior secured” generally means the loan is backed by collateral and ranks ahead of more junior debt. These features can improve recovery prospects, but diversification and manager discipline remain essential because credit risk can never be eliminated. Across all these features, diversification and active credit management can help investors reach the goals of income, resilience and long-term opportunity.

Private credit involves lending money outside the public bond market, usually through loans or other debt agreements negotiated directly with companies. These investments may offer more income than many traditional bonds, but they are often harder to sell quickly because they do not trade often. Results can vary widely, so it is important to understand the fund structure and whether its withdrawal terms fit the long time frame of the loans it holds.

Investors often compare private credit with public debt markets, but the two work in very different ways. Public debt, such as corporate bonds, trades on public exchanges and comes with broad disclosure requirements and significant regulatory oversight. Private credit stays out of those public markets, so fewer details are available and investors commit to holding investments that are much harder to sell before maturity.

Like most debt investments, private credit is designed to generate returns mainly through income rather than large changes in price. Because investors often commit their money for five years or longer, private credit typically offers higher yields than a similar portfolio of publicly traded bonds. At the same time, the main risk remains the same as in other lending investments: borrowers may struggle to repay principal or interest in full.

Private credit funds also tend to update values less often than publicly traded bond funds. As a result, reported returns may appear steady even when the underlying loans have changed in value. That does not mean the investment is free of price risk. Rather, it means the prices changes may appear more slowly.

Private credit can offer higher income than comparably publicly traded debt. In many cases, yields run about 2 to 3 percentage points above public debt with similar characteristics. That extra income can be attractive, but it comes with added risk, including the possibility that a borrower cannot meet its payment obligations.

Liquidity is one of the most important issues to consider in private credit. Because the underlying loans are hard to sell quickly, many funds place limits on when and how much investors can withdraw. Some funds require investors to keep money invested for more than five years, while others allow limited withdrawals, often capped at 5% of net asset value during a set period.

Private credit was once used mainly by large institutions such as pension funds, endowments and insurance companies. Today, accredited individual investors can also gain access through structures such as publicly traded and non-traded Business Development Companies (BDCs) and Interval Funds. Even with that broader access, investors still need to fit private credit into a diversified portfolio with care because these investments offer limited access to cash once money is committed.

Private credit works best when investors approach it with a long-term portfolio commitment. Unlike public stocks or bonds, which are generally easier to sell, private credit depends on a slower process of collecting interest payments and, over time, repaying principal. The higher yield is closely tied to that tradeoff, so investors should be comfortable giving up easy access to liquidity.

A typical private credit time horizon runs from five to ten years. That time frame makes patience essential, especially during periods when markets are unsettled or cash needs change. Investors who commit to private credit should do so with as clear understanding that the investment is built for long-term income, not quick access to funds.

A business development company, or BDC, is an investment vehicle designed to provide capital to small- and mid-sized businesses, often by making private loans. BDCs can trade publicly or be non-traded, and non-traded vehicles may offer limited redemption windows rather than daily liquidity. Because underlying loans can be illiquid, some BDC structures can restrict or pause redemptions during periods of heavy withdrawal demand.

Private credit funds may limit redemptions because the underlying loans are typically multi-year investments that can be difficult to sell quickly without taking discounts. When redemption requests surge, a fund may reduce withdrawals to avoid forced selling of illiquid assets at unfavorable prices. For investors, that means redemption features are often conditional and should be evaluated alongside diversification and credit quality.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.