Tap into life hacks for your savings goals.

Make saving simple.

Put your savings on autopilot to get more of what you want out of life.

See all your finances in one place, breeze through budgets and track spending with our automated tools in the U.S. Bank Mobile App.

Get the app and open a checking account in minutes.

Or text GET APP to 872265 to receive a download link.

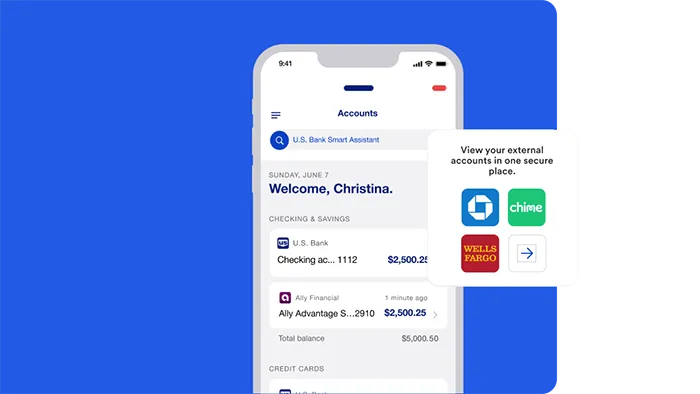

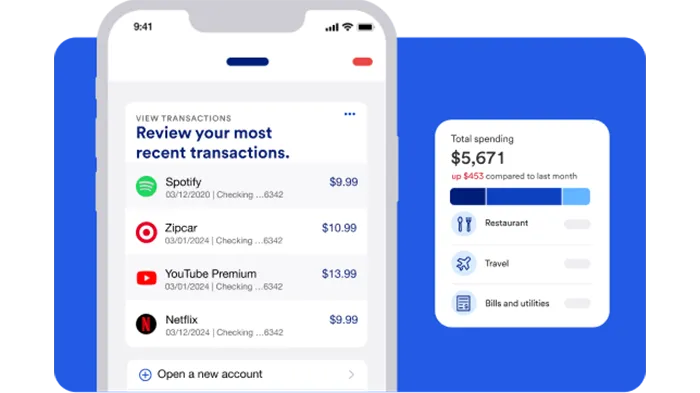

Money management is easy when you can see your U.S. Bank accounts and other bank accounts in one place. Use your secure financial dashboard to link bank accounts – checking, savings, investments, credit cards and more. Your dashboard puts it all together for you.

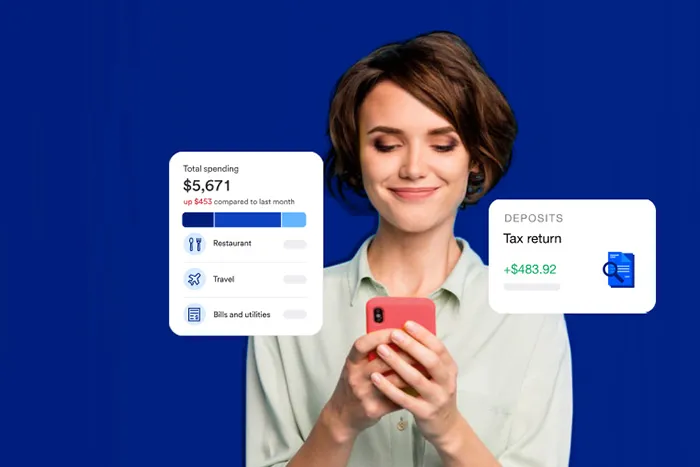

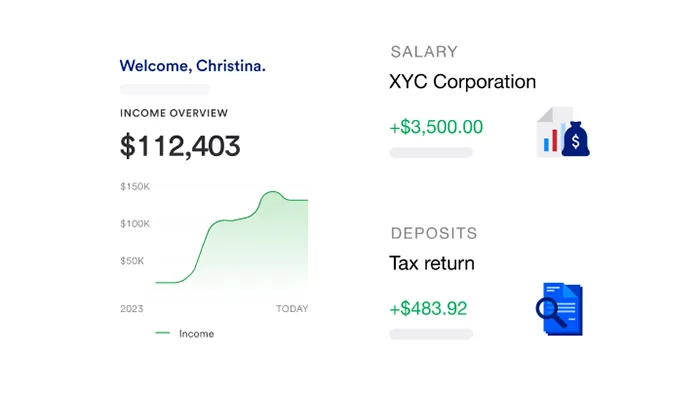

Paint a prettier picture of your cash, income, balances and trends with tracker tools and visualizations.

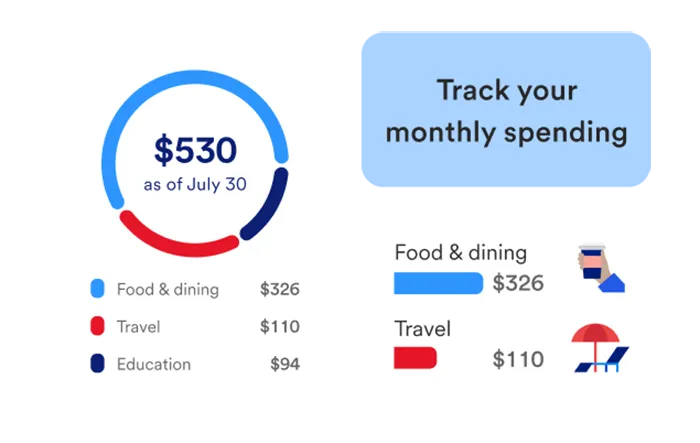

Track expenses to sort transactions by category and set alerts. It also works as a budget tracker so you’ll never overspend.

See upcoming bills and transactions all in one place. Better yet, get reminders to avoid surprises and late fees or see where you might want to cut back.

Bank Smartly® Checking gives you access to these tools and more.

Or text GET APP to 872265 to receive a download link.

Or text GET APP to 872265 to receive a download link.